Chapter 13 Bankruptcy Lawyer Tampa, FL

Chapter 13 Bankruptcy Lawyer Tampa, FL

As a Chapter 13 bankruptcy lawyer in Tampa, FL from Carylon Secor, P.A. will tell you, filing for bankruptcy can be a tough decision for a person to make. Choosing bankruptcy as an option can come with an onslaught of emotions, and debtors will be feeling overwhelmed surrounding both the process and the impact that filing for bankruptcy can have. Crushing debts can impact the scope of the life that you may be living, and fortunately, attorneys like Carolyn Secor, P.A. are prepared with the experience needed for those in need of a solution. We know that you will have many questions, which is why we are available to meet with you to offer the solutions you need.

What is Chapter 13 bankruptcy?

Chapter 13 is often referred to as a “wage earner’s plan.” This is a standard solution for a debtor with an income that exceeds the state’s median income levels. However, it’s essential to be aware that the debts of a person filing for Chapter 13 cannot exceed more than a certain amount. When filing for Chapter 13, the debtor will develop a repayment plan that allows them to pay back their debts over time.

How will I know that Chapter 13 is the right option for me?

Identifying the right chapter to file for is a huge decision to make, and knowing how to move forward may take the assistance of our bankruptcy lawyer. This form of bankruptcy may be the right option if:

- You are making a steady income that exceeds the state’s median

- You have assets you are looking to keep

- You are looking to retain your home

- You are behind on your mortgage and need time to catch up

- Your assets equate to more than the exemptions that are available to you

If I file for Chapter 13, am I able to keep my home?

It’s possible that by filing for Chapter 13 that you will be able to keep your home. In some situations, by filing for Chapter 13, you will be able to retain your housing. Chapter 13 can allow the opportunity to keep your property while catching up on any arrears.

How long does it take to put together a plan for Chapter 13?

Typically Chapter 13 bankruptcy will take longer to file and resolve than a Chapter 7 filing. Chapter 13 is different in that a resolution is reached over a much more extended period. Debtors create work to develop a repayment plan over 3-5 years. This is the amount of time needed before all debts through Chapter 13 are paid off, and bankruptcy is resolved.

When will my credit rebound from Chapter 13?

While it can take 3-5 years for Chapter 13 to resolve, the process of rebuilding credit takes place immediately after filing for Chapter 13. Initially, your credit may take a hit after filing. Still, you will likely see an improvement over time, especially if you make an effort to make sound financial decisions to rebuild your credit moving forward.

How is Chapter 13 Bankruptcy different from Chapter 7 Bankruptcy?

One of the primary distinctions between Chapter 13 bankruptcy and Chapter 7 bankruptcy involves eligibility. Both of these chapters of the Bankruptcy Code facilitate personal bankruptcy filings (ie: bankruptcies filed by individuals and families that don’t involve business bankruptcy). However, not every individual and family is eligible to file for both kinds of personal bankruptcy. Chapter 7 bankruptcy is an option reserved for those who don’t earn much income. The law imposes a so-called “means test” upon those who apply for debt relief under Chapter 7. If a filer earns too much income to qualify for Chapter 7 bankruptcy, they will be compelled to file for Chapter 13 bankruptcy instead.

Oftentimes, filing for Chapter 7 bankruptcy is a preferable option for those who are eligible, for several reasons. Before noting them, however, it’s important to understand that not every filer eligible to take advantage of this option should pursue it. When you meet with the experienced Florida legal team at Carolyn Secor, P.A., our firm’s Tampa, FL Chapter 13 bankruptcy lawyer will let you know whether your unique situation would be better served by either filing for Chapter 13 bankruptcy or pursuing a non-bankruptcy debt relief option. No debt solution is “one-size-fits-all” and it is therefore important to become fully informed about all options available to you before committing to a plan of action.

Why is Chapter 7 bankruptcy – usually – a better option for those who are eligible to take advantage of this opportunity? Unlike Chapter 13 bankruptcy, which reorganizes debt and then commits a filer to a 3-to-5-year repayment plan, the Chapter 7 bankruptcy process erases eligible, unsecured debt in as little as 90 days or so. There is no mandatory repayment schedule attached to this debt relief option. Instead, filers are granted access to a fresh financial start with very few strings attached.

If I’m eligible for Chapter 7 relief, would filing for Chapter 13 ever be a better option?

If Chapter 7 bankruptcy doesn’t require a filer to repay their eligible debts, why would Chapter 13 ever be a preferable option? Chapter 7 bankruptcy is commonly referred to as “liquidation bankruptcy.” This is because the trustee assigned to a Chapter 7 case is empowered to sell off a filer’s non-exempt assets so that they can forward the proceeds of this sale to the filer’s creditors. Most Chapter 7 filers don’t own enough valuable non-exempt assets that this is a risk worth worrying about.

However, some Chapter 7 filers don’t earn a lot of income but do own some valuable non-exempt property. If this describes your situation, our firm’s bankruptcy lawyer will be able to evaluate your property and compare it to the exemption laws available to you. Once you have a strong sense of whether property that has meaning and/or value to your family may be at risk of being sold via a Chapter 7 bankruptcy proceeding, you can make an informed decision about whether filing for Chapter 13 bankruptcy may be a preferable alternative.

What You Should Know About Avoiding Personal Bankruptcy

As a small business owner, there are several things that could get confused between your personal life and your professional life. Fortunately, with the right help, you can effectively separate the two lives so they don’t affect each other. If you’re worried about personal bankruptcy because of financial decisions made in your business, there are some things you should know.

Setting Up Your Entity Correctly

When you set your business up as an entity, you have to do it correctly in order to protect your personal assets. If your business is a sole proprietorship, your personal assets are totally exposed and could face a lawsuit. An LLC or S corp are better options to keep your personal and professional assets separate, and to keep your personal assets protected.

Maintaining the Corporate Veil

Even when you set up your entity correctly, you have to be strict about maintaining the corporate veil. This means that you create separate bank accounts for your personal finances and your business finances. You need to keep your company name on all professional documents, and only your personal name on personal documents. You should never take out a second mortgage on your home to help your business, and borrowing money from your business to take care of personal financial issues should be avoided.

Purchasing Insurance

Every aspect of your business should be properly covered by insurance so nobody who files a claim against your business would even consider going after your personal assets. There are different types of insurance policies for different types of companies, so you should be sure your policy covers all the specific risks associated with your business.

Using Appropriate Procedures

If you conduct your business fraudulently or negligently in any way, it becomes a lot easier for someone to attack your personal assets. One thing you can do to avoid this is to always use appropriate procedures and contracts. Get signatures on everything and be sure you include a lawyer in the legal processes of your business.

Splitting Ownership

If you are married and one spouse has a riskier occupation, you can split legal ownership of your personal assets so they are protected better. For example, if your wife is a doctor and could be sued for malpractice, you could protect your home and cars by putting them in your name instead.

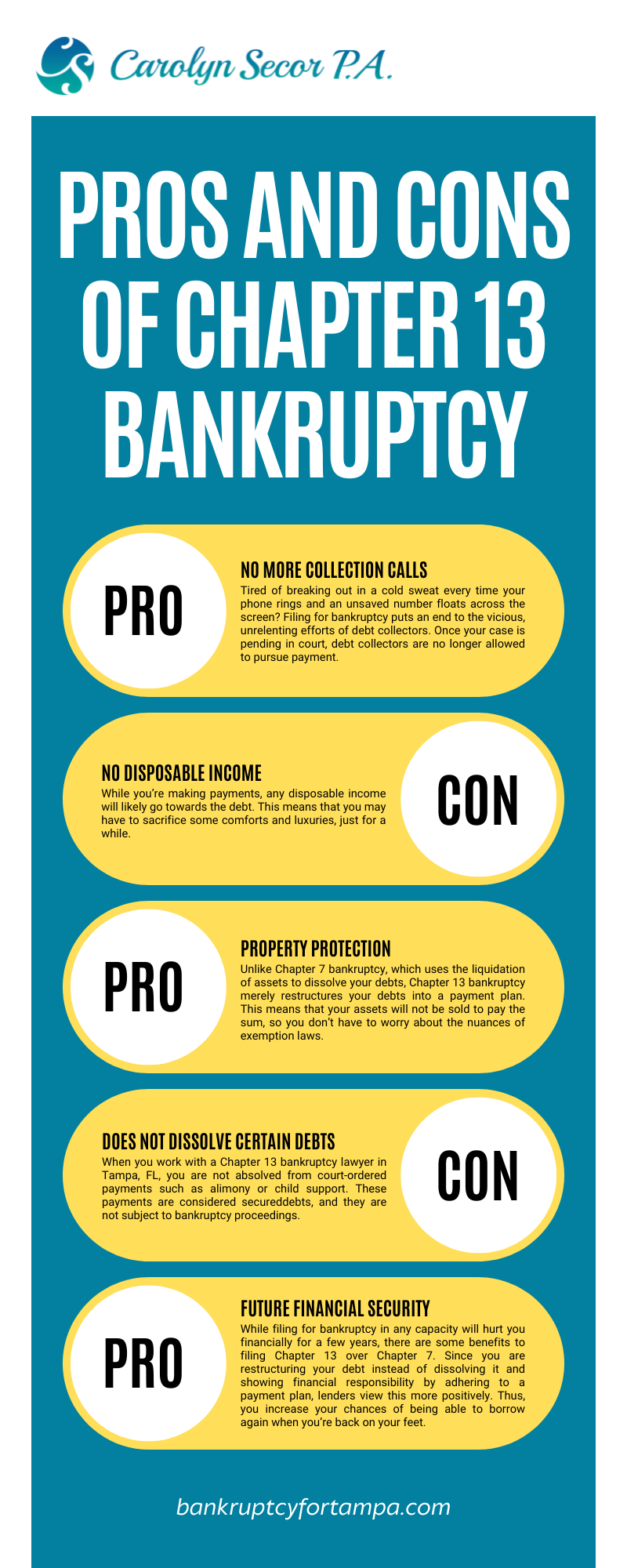

The Pros and Cons of Chapter 13 Bankruptcy

Debt is hard to talk about. When you’re facing bankruptcy, you may feel scared, anxious and even ashamed of your situation. You are not alone. Americans have an average credit card debt of over $6,000. As odd as it may seem, filing for bankruptcy is the first step towards a financially secure future. If you’re ready to file for Chapter 13 bankruptcy, here are a few pros and cons you should be aware of.

Pro: No More Collection Calls

Tired of breaking out in a cold sweat every time your phone rings and an unsaved number floats across the screen? Filing for bankruptcy puts an end to the vicious, unrelenting efforts of debt collectors. Once your case is pending in court, debt collectors are no longer allowed to pursue payment.

Additionally, if you have legal representation, the debt collector is required to contact your lawyer, not you. This is why it is best to immediately seek out and inform collectors you have retained a Chapter 13 bankruptcy lawyer in Tampa, FL. If debt collectors continue to contact you, they’re breaking the law, and you can report them to the Federal Trade Commission.

Pro: Property Protection

Unlike Chapter 7 bankruptcy, which uses the liquidation of assets to dissolve your debts, Chapter 13 bankruptcy merely restructures your debts into a payment plan. This means that your assets will not be sold to pay the sum, so you don’t have to worry about the nuances of exemption laws.

Pro: Future Financial Security

While filing for bankruptcy in any capacity will hurt you financially for a few years, there are some benefits to filing Chapter 13 over Chapter 7. Since you are restructuring your debt instead of dissolving it and showing financial responsibility by adhering to a payment plan, lenders view this more positively. Thus, you increase your chances of being able to borrow again when you’re back on your feet.

Con: No Disposable Income

While you’re making payments, any disposable income will likely go towards the debt. This means that you may have to sacrifice some comforts and luxuries, just for a while.

Con: Does Not Dissolve Certain Debts

When you work with a Chapter 13 bankruptcy lawyer in Tampa, FL, you are not absolved from court-ordered payments such as alimony or child support. These payments are considered secureddebts, and they are not subject to bankruptcy proceedings.

Filing for bankruptcy is a big decision, but it just could be the best decision you ever made to start building a better life for yourself. Don’t let the stigma scare you off from the future you could have, and find out if a Chapter 13 bankruptcy lawyer in Tampa, FL, is right for you.

How to Prepare For Meeting With Your Chapter 13 Bankruptcy Lawyer

Filing bankruptcy is a serious undertaking and requires following the legal process outlined in the bankruptcy code. You will need to disclose various personal details in your bankruptcy schedules. Here are some things you will need to gather information about before meeting with your bankruptcy attorney.

Real Estate

You must list any real property you have an ownership interest in and the type of ownership interest you have. Your Chapter 13 bankruptcy lawyer in Tampa, FL, will include all real property on Schedule A, including the value of the property and any debts owed. Before meeting with your attorney with Carolyn Secor, PA, you will want to gather as many records about the property that are available to you. You can start with a copy of the tax assessment from the locality. If you have a recent appraisal, you will need to bring that. In addition to documents that show the property’s value, you will need to bring copies of any mortgage statements for loans that you have on the property.

Income and Expenses

You will also have to provide a schedule of your income and monthly expenses. When you meet with your Chapter 13 bankruptcy lawyer in Tampa, FL, you should bring copies of your paystubs and investment and retirement account statements that document your monthly income. You must disclose all of your income, so if you have other sources of income, you will need to tell your attorney with the firm of Carolyn Secor, PA, about any other income you may have.

For your expenses, you should go through your bank account and determine what you pay on average for your regular household bills. You will also list credit card payments, other consumer loan payments, student loan payments and car loan payments. You should bring copies of your three most recent statements from your creditors for these expenses.

Personal Property

You must file a listing of all your personal property. Before meeting with your Chapter 13 bankruptcy lawyer in Tampa, FL, you should make a list of all the personal property you own. This list should include your furniture, audiovisual equipment, appliances, clothing, coin collection, guns and jewelry. You will have to assign a value to your property on your bankruptcy schedules.

Filing Chapter 13 is a comprehensive undertaking, but your attorney with the firm of Carolyn Secor, PA, will be able to guide you through the process.

4 Common FAQs About Chapter 13 Bankruptcy

Are you struggling to pay off your debt? Are you so deeply in debt you believe it would take years to pay off your bills? If you answered yes to the previous questions, you may be considering filing chapter 13 bankruptcy. Choosing to file for bankruptcy is a major decision that shouldn’t be taken lightly, but if you think it is right for you, you will certainly want to hire a chapter 13 bankruptcy lawyer in Tampa, FL at Carolyn Secor, PA to help guide you in the right direction. Filing for bankruptcy can be confusing, and you probably have a lot of questions. Here are some FAQs about chapter 13 bankruptcy along with some helpful answers.

1. How Are Chapter 13 and Chapter 7 Bankruptcy different?

When a person files for chapter 7, all of their debts will be discharged and their creditors will receive no payments. Conversely, when a person files for chapter 13 bankruptcy, they will be required to make payments on the debt for three to five years. In other words, chapter 13 is a sort of repayment plan that results in creditors recovering some of the debt they are owed. Your chapter 13 bankruptcy lawyer in Tampa, FL can help you create a plan.

2. Will I Need to Pay All My Debts Through the Chapter 13 plan?

No. Any secured debt you are current on, such as your mortgage or car payments, can be paid to the lender directly. All other unsecured debt you are not current on must be paid through the plan. Depending on your amount of assets and disposable income, you may only have to pay a small percentage of your unsecured debt via the plan. Carolyn Secor, PA can help you determine the details of your payment plan.

3. Do Creditors Have to Approve My Bankruptcy Plan?

No. The bankruptcy judge is the only person who must approve of your plan. However, if your plan is correctly prepared and takes all of your debt into consideration, they shouldn’t have any problems. In theory, even if a creditor does oppose your plan, it is still up to the judge whether it should be implemented.

4. Will Collection Activity Against Me Cease After I File Chapter 13 Bankruptcy?

After you file bankruptcy, an “automatic stay” will be imposed on your creditors. This prevents any further wage garnishments, court cases, foreclosures, repossessions, etc. The stay remains effective throughout the duration of your bankruptcy unless a creditor has a legitimate cause to petition the court to remove the stay. As long as you make your required payments, there should be no reason for them to file such a petition.

Legal Assistance Is Available

Debts can impact nearly every aspect of a person’s life. When you are a person who is earning a living that is beyond the state’s median standard, you may qualify for Chapter 13 as a solution. While the decision to file for bankruptcy wasn’t an easy one to make, Carylon Secor, P.A. is confident that you will be able to experience relief from the direction that we can provide you. Take control over your debt by scheduling a consultation with our Chapter 13 bankruptcy lawyer in Tampa, Florida from Carolyn Secor, P.A. as soon as possible.

Client Review

"Ms Secor and Sam were with me during a very dark time. They helped me through a mess I made by trying to do this on my own. She was extremely knowledgeable and had my best interest in mind. Thank you very much!!!"

Kellie Almond